Our Products

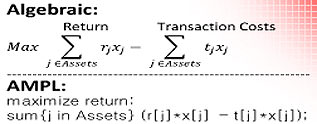

Algebraic Modelling Language Family

Sentiment Analysis

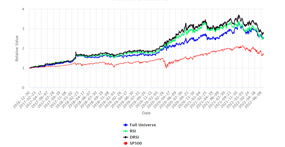

Financial Analytics for Asset Allocation

Whitepapers

Comparative Analysis of NLP Approaches for Earnings Calls

The field of natural language processing (NLP) has evolved significantly in recent years. In this chapter we consider two leading and well-established methodologies, namely…

Asset Allocation Strategies: Enhanced by News

The explosive development of electronic media has brought to the market participants thousands of pieces of financial news which are released on different platforms every day.

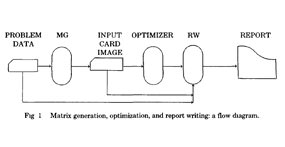

UIMP: User Interface for Mathematical Programming

UIMP is a matrix-generator report-writer system designed to aid the realization (generation) of mathematical programming models and also the analysis-reporting of the solutions of…

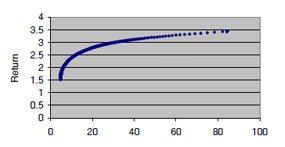

Portfolio Optimization

This white paper introduces Markowitz mean-variance model with a general overview and sets out to explain why and how the finance industry has fully embraced this as a method of choice for portfolio planning.

Want to see a demonstration or want to know more about our products?

Our Services

Training

OptiRisk Systems offers training in optimization, risk analysis and other quantitative financial tools. We have highly experienced professionals on the teaching faculty…

Projects & Consultancy

We are aware a client is usually interested in having a capped budget for consultancy services. Thus, for a Proof of Concept (POC), the initial step of full client…

AMPLDev Cloud

AMPLDev cloud provides instant access to guaranteed up-to-date versions of our software suite. Removing all installation processes, AMPLDev Cloud directly links…

Trade SES

Sentiment Enhanced Signals (SES) optimizes your equity portfolio composition using a powerful optimization model known as Second Order Stochastic Dominance (SSD)…

News & Events

Application of Generative AI, LLMs and NLP in Trading, Fund Management and Risk Control

This two-part webinar is of 60-minutes duration each – it is presented in the format of a fireside chat with a small panel of subject experts....

Utilizing Sentiment Analysis for Effective Assets Allocation, May 31, 2023

Alexandria Technology is a leading provider of financial sentiment data and OptiRisk Systems is well known for financial models for asset allocation enhanced by sentiment. Alexandria and OptiRisk are presenting the resul...

Financial Evolution: AI, Machine Learning & Sentiment Analysis, Zurich, November 03, 2022

Innovations in Finance and harnessing of Technology have resulted in making the term Fintech a portmanteau word. In the evolution of the BFSI sector Fintech has assumed a pivotal role; but it also had an impact on tradit...